When clients come into our office and say, “I just want to make sure my kids get everything easily,” the next question is almost always this:

Should I name a beneficiary or add a transfer-on-death clause?

They sound similar. They are not the same. And from a tax standpoint, the differences matter.

Let’s break it down in plain English.

What Is a Beneficiary?

A beneficiary is a person (or a trust or charity) you name to receive an asset upon your death. This is most common with:

Retirement accounts such as 401k and IRA

Life insurance policies

Annuities

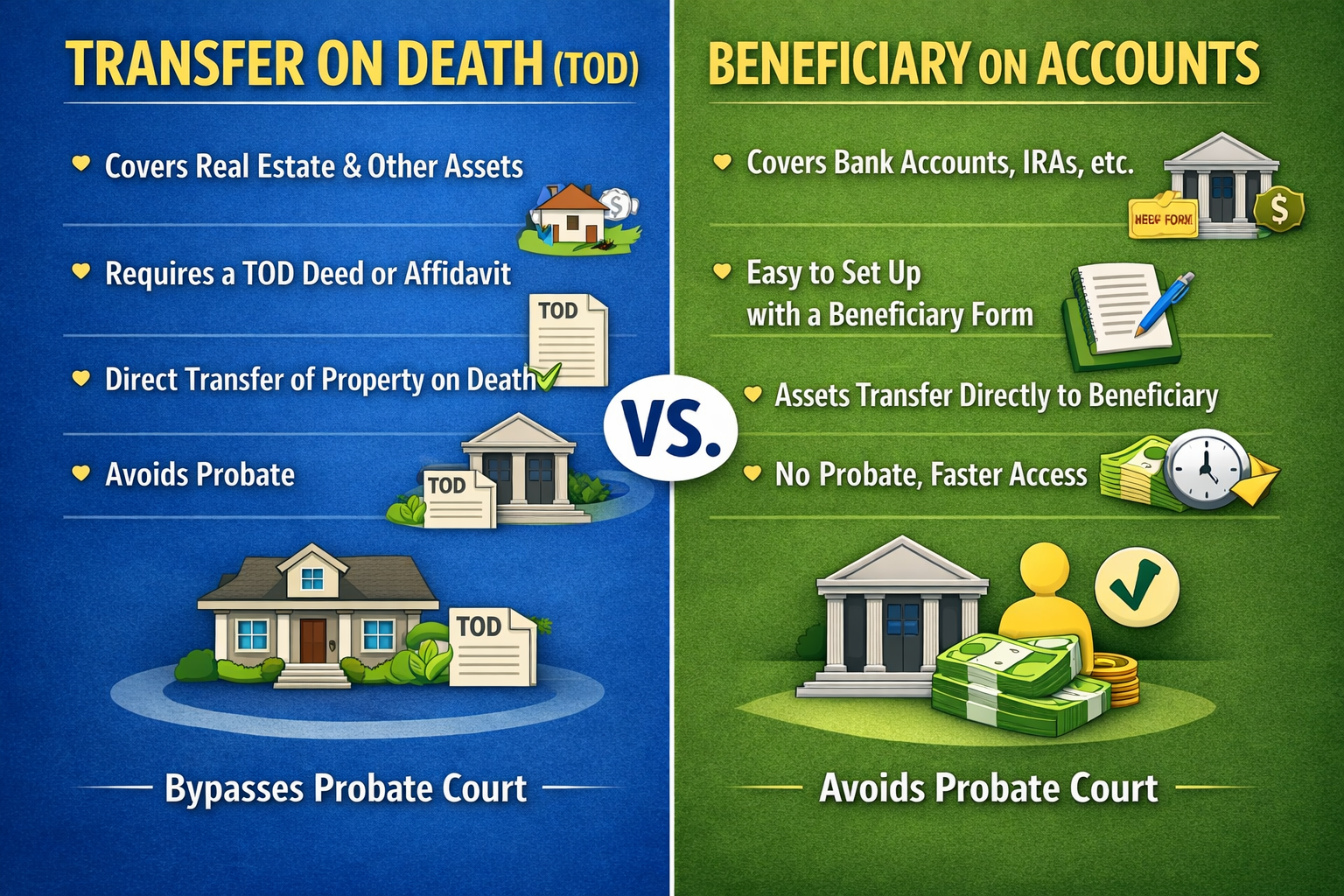

These accounts pass directly to the named beneficiary. They do not go through probate. That means faster access and less court involvement.

Tax Treatment of Beneficiary Accounts

Here is where it gets important.

Retirement Accounts

If your child inherits your traditional IRA, they generally must pay income tax as they withdraw the funds. Under current rules, most non-spouse beneficiaries must withdraw the entire account within 10 years of death.

Spouses have more flexibility. A surviving spouse can roll the IRA into their own IRA and stretch distributions over their lifetime.

The key point: there is no step-up in basis on traditional retirement accounts. Every pre-tax dollar withdrawn is taxable income.

NEVER make a trust the beneficiary of your IRA or 401K!

Life Insurance

Life insurance proceeds paid to a beneficiary are generally income tax-free. That makes it one of the cleanest wealth-transfer tools available from an income-tax standpoint.

Estate Tax

Naming a beneficiary does not remove the asset from your taxable estate. For federal estate tax purposes, retirement accounts and life insurance you own are typically included in your estate. However, for 2025, the federal estate tax exemption is over $ 13 million per person, so most families are not affected.

When Is a Beneficiary the Best Option?

A beneficiary designation is usually best for:

Retirement accounts

Life insurance policies

Situations where you want quick, probate-free access

When you want to name contingent beneficiaries

It is simple, efficient, and often the only proper method for certain accounts.

What Is Transfer on Death (TOD)?

Transfer on death is a registration you add to certain assets, most commonly:

Brokerage accounts

Individual stocks or bonds

Some bank accounts

In many states, real estate

You still own and control the asset during your lifetime. When you pass away, the asset automatically transfers to the named TOD beneficiary without probate.

Think of it as a beneficiary designation for non-retirement investment assets.

Tax Treatment of TOD Assets

Here is where TOD often shines.

Step-Up in Basis

When someone inherits a taxable investment account through a TOD designation, they generally receive a step-up in basis to the fair market value on the date of death.

That means if you bought stock for 50,000 and it is worth 200,000 when you pass away, your beneficiary’s new basis is 200,000.

If they sell it shortly after inheriting it for 200,000, there is little to no capital gains tax.

Compare that to retirement accounts, where every dollar is taxable when withdrawn.

Income Tax

There is no income tax triggered at death when assets are transferred through TOD. Taxes only apply if and when the beneficiary sells the inherited asset.

Estate Tax

Just like beneficiary designations, TOD assets are still included in your estate for estate tax purposes.

When Is Transfer on Death the Best Option?

TOD is often best for:

Taxable brokerage accounts

Appreciated stock positions

Real estate in states that allow TOD deeds

Clients who want to avoid probate but preserve the step-up in basis

If your goal is to pass highly appreciated investments to your children in the most tax-efficient way, TOD on a taxable brokerage account can be extremely powerful.

A Simple Example

Let’s compare two assets:

Asset 1: Traditional IRA worth 500,000

Asset 2: Brokerage account worth 500,000 with original cost of 100,000

If your daughter inherits the IRA as a beneficiary, she must withdraw the funds within 10 years and pay ordinary income tax on each dollar. (At the top of your adult child’s earning time, they will need to take out the money from your retirement— think HIGH taxes)

If she inherits the brokerage account through TOD, her basis becomes 500,000. If she sells it for 500,000, she owes no capital gains tax. (Money goes to your daughter- not the IRS)

Same dollar value. Very different tax result.

Common Mistakes We See:

Forgetting to update beneficiary forms after divorce– CHECK IT NOW! Especially if you children have become adults!

Naming minors directly without planning (big mistake- never name a minor)

Assuming a will overrides a beneficiary or TOD designation

Leaving large retirement accounts to high-income children without tax planning

Remember this: beneficiary and TOD designations override your will. If the form says your ex-spouse inherits your IRA, that is likely who will receive it.

The Bottom Line

Beneficiary designations are essential for retirement accounts and life insurance. They provide efficiency and probate avoidance, but retirement accounts come with built-in income tax.

Transfer on death designations are powerful for taxable investments because they combine probate avoidance with a step-up in basis.

Both tools are simple to implement. Both are powerful when used correctly. And both deserve a careful review as part of your overall estate and tax plan.

Remember never just add your child’s name to your accounts- this could cause you to lose it all if your child is in an accident or get’s divorced!

If you have not reviewed your beneficiary and TOD designations in the last few years, this is your friendly nudge from your CPA.

Remember your CPA is not just a pretty face- they are your financial partner– or they should be!